China + 1 strategy: Shift of Paper Manufacturing from China to other developing Countries India, Vietnam, Indonesia etc. It is up to us how we en-cash this opportunity.

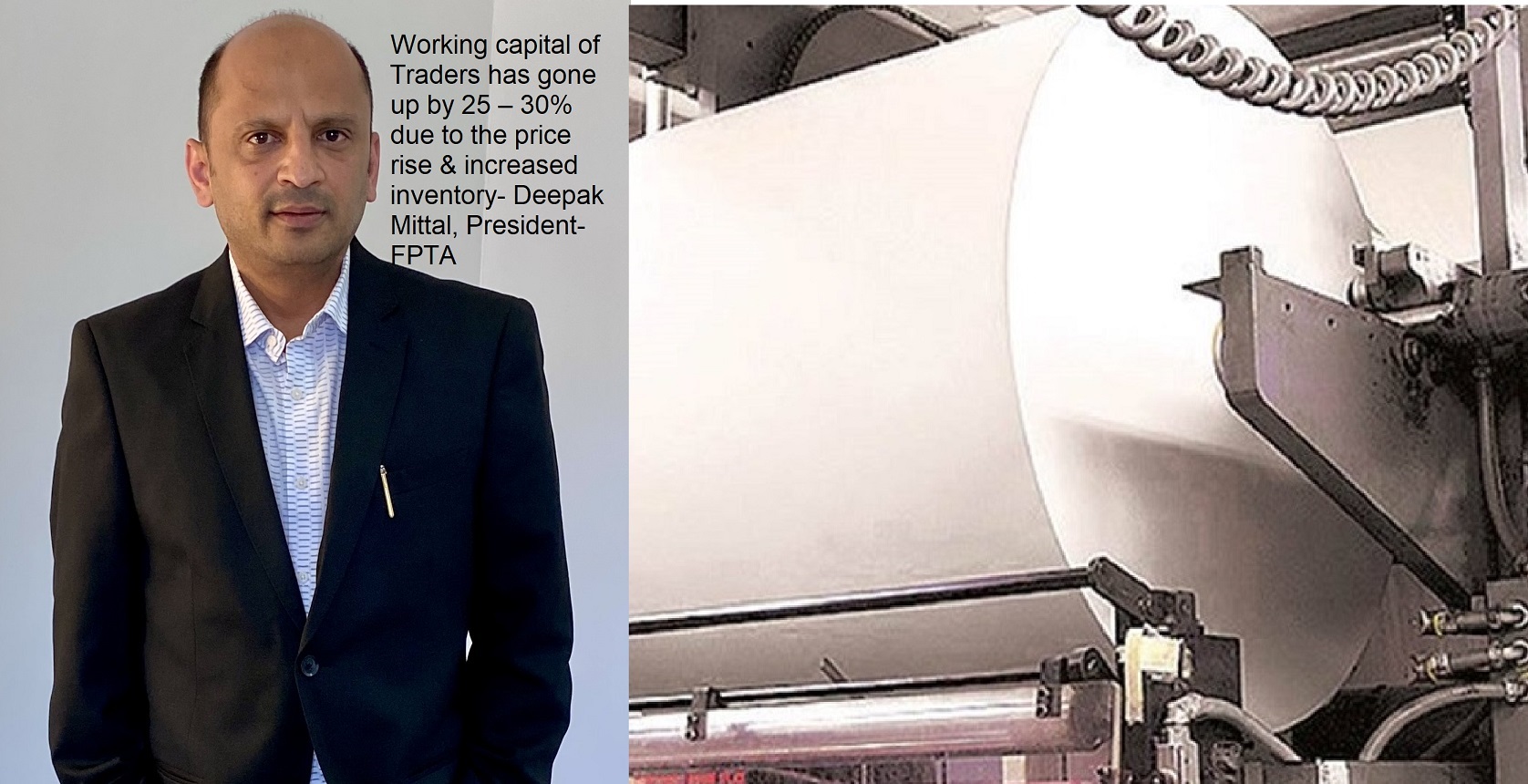

-It is estimated that the working capital of Traders has gone up by 25 – 30% due to the price rise & increased inventory as a result of disruption in supply chain.

-The estimated turnover of the 6,000 plus strong trader is around INR 70,000 crores

Mr. Deepak Mittal becomes the 60th president of the Federation of Paper Traders Association (FPTA) for the year 2021-2022. Mr. Mittal shares his views on the current situation of the Indian Paper Industry exclusively with The Pulp and Paper Times. Here are his views:

November 2021 | The Pulp and Paper Times:

Paper is an indispensable part of our civilization. Paper is versatile and a technological marvel. It is capable of creating delicate details and yet it can be incredibly sturdy. Paper is recyclable, biodegradable, and reusable substance whose raw material wood is renewable.

The versatility of paper comes to our support in a variety of forms in today’s present life. Paperboard and packaging paper is crucial for almost all goods, especially all kinds of essential goods, FMCG, pharmaceuticals, textiles, food products, soaps, milk cartons, hygiene products, and more. Universal literacy is unthinkable without paper.

The paper and board industry world over is diversifying and responding to an increasingly globalised marketplace. Global megatrends are reshaping the markets faster than ever.

Currently the worldwide supply of paper and board is almost 420 million tonnes. During the last 20 years China has taken the lead in terms of production volumes surpassing the US. The size of Chinese market is approx.. 125 Mn. Tons - approximately 28 – 30% of the world’s demand. India is approx.. 20 Mn. Tons. Interesting feature is that both the Countries have the same population but China is 6 – 7 times of India’s size. The Per Capita consumption of Paper in India is 14 Kgs as against global average of 57 Kgs. In Europe the largest volumes are produced in Germany, Finland and Sweden.

It is important and interesting to find that there are disruptive technologies that are impacting the evolution of the paper and board industry.

E-commerce retail sales are continuing to rocket. US and China are currently the two largest e-commerce markets. It is estimated by Smithers that around $355 billion of all retail sales in China will be conducted over e-commerce, and that over 15% of US sales will use this means in the same year.

Internet shopping by consumers is a key driver to the demand for new packaging solutions. Consumer packaging, such as cartonboards, serves the needs of both on-the-shelf display and advertising. It also acts as carriers of small-size goods. This trend is creating positive growth rates in the demand for corrugated boxes, Carton Boards and its raw materials.

There is a huge shift to Lightweight Packaging Boards (Virgin Packaging Boards) as they offer multiple benefits depending on the end-use. In luxury cartonboards lighter weight boards can improve brand value. Demand for lighter-weight packaging board will continue to grow due to the many advantages it offers.The principal gains from switching to a lighter weight board are: Reduced pulp costs, less weight in logistics, reduced costs and CO2 emissions, enabling more primary packs per pallet, and less weight at end of life.

Recyclability is becoming more of a key requirement for consumer packaging products. Recyclable barrier coatings will develop fast over the next ten years, but costs will be a limiting factor.

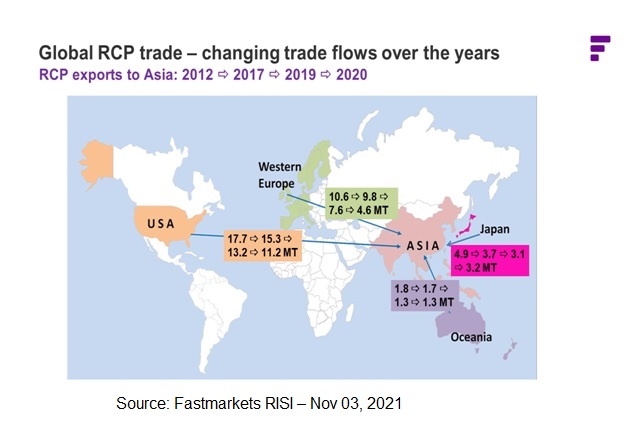

Global recovered paper trade is being transformed by changing policy and consumer demand. Pandemic-induced demand for packaging and import regulations in key regions are driving huge changes in the recovered paper (RCP) market. The Asian recovered paper imports have declined in the last few years because of China’s RCP import ban and other Asian countries’ RCP import restrictions, as well as the complications brought by the pandemic. The global RCP trade volume remains high, with China and the rest of Asia being the key players that influences global market movements. China officially stopped importing RCP from the beginning of 2020, and yet it remains one of the most important player in the global recycled fibre market. International Trade in RCP will continue to be an important factor in the changing global market dynamics.

The paper industry is reinventing itself so as to provide an environment-friendly alternative in different spheres of life. Being environment friendly and sustainable, the demand for paper in most areas will only grow.

The domestic paper & paper products industry and trade were one of the worst affected industries due to the outbreak of Covid-19 pandemic. The lockdown imposed in the last week of March 2020 resulted in the closure of operations. While paper industry’s operations resumed with reduced capacities as restrictions eased, challenges remained in terms of logistics disruption and migration of labour. In addition to this, trade remaining closed, subdued demand from consumers also impacted sales. Closure of education institutions, adoption of work from home by offices, muted demand for printing of newspapers among others disturbed the consumption of paper & paper products. Moreover, subdued demand also had an impact on the prices of paper & paper products which further affected the revenues.

There is little doubt that the domestic paper industry and trade has passed through a difficult time during the last year. The nationwide lockdown last year led to disruption of both inward and outward supply chains. The sporadic lockdowns and mobility restrictions impacted the fragile recovery.

The demand for writing and printing paper continues to be severely impacted due to the closure of educational institutes and offices. The Scholastic Sector contributes close to 60% of the Writing & Printing Paper demand. Last year due to the stringent lock downs imposed in India, the Writing & Printing segment shrank approximately by 35%and it was one of the worst performing segments globally. Literacy levels in India still need to improve significantly.

Newsprint, which was already in the doldrums before the pandemic, has been badly impacted due to a reduction in newspaper circulation, and fall in advertising revenue. This resulted in curtailment of pages leading to reduced demand.

Tissue paper helps in improving hygienic conditions. The away-from-home demand for tissue has been adversely impacted, with many offices, and commercial establishments closed across the country, with work-from-home continuing even after the lifting of lockdowns.

There has been some recovery in few segments with the easing of restrictions, notably packaging paper and paperboard, with the demand picking-up. The Packaging segment size is approx.. 12 Mn.tons in India and growing at a rate of 6 – 8% annually. The current demand is running at higherthan pre Covid levels. There has been significant jump in exports of Packaging grades of Paper & Paper Boards due to the ban imposed by China on RCP.

The revival of economic activity, expected reopening of educational institutions and offices, uptick in tourism, opening up of restaurants and hotels, and service industry moving back towards normalcy, would certainly lead to increase in consumption and demand for paper. Growth is bound to take place as the Indian economy grows. Also with the world looking at China + 1 strategy, there is going to be a shift of Paper Manufacturing from China to other developing Countries India, Vietnam, Indonesia etc. It is up to us how we en-cash this opportunity.

Also, the ban on single-use plastic is going to be a mega trend over the next decade for the Paper Industry as Paper is the most eco-friendly alternative to Plastic.

The major challenge before the domestic industry is the availability of raw materials in sufficient quantity and at globally competitive prices. India is a fibre deficient country, whether wood or agriculture residue or recycled fibre/waste paper. Since the raw material is a major cost component of the production of paper, this single factor adversely impacts the cost competitiveness of the Indian industry as compared to other competing countries.

The Trade is also going through its challenges in terms of significant rise of working capital. It is estimated that the working capital of Traders has gone up by 25 – 30% due to the price rise & increased inventory as a result of disruption in supply chain. Further, as a result of 6 – 8% expected growth every year, the Trade needs to invest close to 1200 – 1500 Cr. to take care of the growth. But the good part is that the business is on a growth path.

Consumers are becoming increasingly conscious of their impact on the environment. The majority of Indian consumers believe that the domestic recycling rate of paper isn’t very high. This consumer awareness needs to be a matter of concern for the domestic players considering paper is, in fact, one of the most recycled materials in the world with a recycling rate of around 74%.

The print and paper industry is surrounded by myths, most of which are rooted in historical misconceptions about paper’s impact on forests. For many years, service providers have reinforced these environmental myths in their efforts to move consumers to digital communications. Greenwashing has become a standard procedure. The need to bust these myths and raise awareness of paper’s sustainability is now more important than ever.

Being environment friendly and sustainable, the demand for paper in most areas will only grow. Modern life is made possible with versatile paper coming to our rescue in a variety of forms. Paperboard and packaging paper is crucial for almost all goods, especially all kinds of essential goods, FMCG, pharmaceuticals, textiles, food products, soaps, milk cartons, hygiene products, and more.

Paper is green, and it is never too late to switch to paper-based alternatives for the larger good of the environment. Paper is one of the most environmentally sustainable products as it is biodegradable, recyclable and is produced from sources, which are renewable and sustainable.

The paper trade has been a less celebrated segment of Indian distributive and retail sector. However, the economic and social importance of the paper trader is unique. The estimated turnover of the 6,000 plus strong trader is around INR 70,000 crores. The trade provides direct employment to 25,000 persons, and indirectly to around100,000. The trade supports the vital national objectives of education, employment generation and availability of goods for all.

Web Title:

China plus 1 strategy Shift of Paper Manufacturing from China to other developing Countries India

Join WhatsApp Group

Join WhatsApp Group Join Telegram Channel

Join Telegram Channel Join YouTube Channel

Join YouTube Channel Join Job Channel (View | Submit Jobs)

Join Job Channel (View | Submit Jobs)